India's Budget 2025-2026: Key Highlights, Reforms, and Economic Strategies for Growth

Overview: India's Budget 2025-2026 emphasizes transformative growth through agriculture, MSMEs, and investment initiatives, aiming for sustainable development, job creation, and global competitiveness. The government’s strategic focus on fiscal reforms and technological advancement promises a robust economic future.

The Union Budget for 2025-2026 was introduced by Finance Minister Nirmala Sitharaman during February 1, 2025 to start a significant economic period for India. The Budget provides India with its crucial transformation plan by prioritizing inclusive augmentation and job creation and technological development alongside international market expansion. The government launched crucial strategic initiatives to work on agriculture and MSMEs alongside investments and exports because these sectors aim to strengthen both workforce capability and financial strength. India aims to solve its internal demands through these vital domains to expand its worldwide reach.

Budget Estimates:

- The money received from all sources except borrowings reached ₹34.96 lakh crore.

- Total expenditure: ₹50.65 lakh crore

- Net tax receipts: ₹28.37 lakh crore

- Fiscal deficit: 4.4% of GDP

- Gross market borrowings: ₹14.82 lakh crore

- Capex expenditure: ₹11.21 lakh crore (3.1% of GDP)

New tax slabs

- The new tax system grants middle-class taxpayers total tax exemption if their monthly earnings stay below ₹1 lakh (annual income below ₹12 lakh).

- The Salaried Class can escape income tax obligations if their yearly income does not exceed ₹12.75 lakh because of the standard deduction amounting to ₹75,000.

Revised Income Tax Slabs:

- ₹0–4 Lakh: NIL

- ₹4–8 Lakh: 5%

- ₹8–12 Lakh: 10%

- ₹12–16 Lakh: 15%

- ₹16–20 Lakh: 20%

- ₹20–24 Lakh: 25%

- Above ₹24 Lakh: 30%

The government improved taxation deductions for older citizens and increased the limits which trigger TDS on rental transactions and TCS obligations.

Focus on Growth Engines:

The "Focus on Growth Engines" component in the 2025-2026 Budget summarizes essential sectors especially agriculture, MSMEs and investment that drive India's economic expansion. The government develops these sectors through productivity growth and business support and innovation promotion in order to establish job markets which encourage economic self-provider and global market competitiveness. The government has implemented these programs which will lead India toward sustainable economic development throughout the next decade.

Agriculture:

- The Prime Minister Dhan-Dhaanya Krishi Yojana received launch funding to increase agricultural productivity by offering modified Kisan Credit Card (KCC) Scheme loans of up to ₹5 lakh.

- Initiative for Aatmanirbharta in Pulses will apply special emphasis to pulse production through a six-year national mission.

- Comprehensive programs for vegetables, fruits, and cotton productivity.

MSMEs:

- Enhanced credit availability with guarantee cover for MSMEs (from ₹5 crore to ₹10 crore).

- A new scheme enables initial women business owners from SC/ST communities to obtain financing worth up to ₹2 crore.

- The government plans to create a National Manufacturing Mission which will support every size of manufacturing industry.

Investment:

- Atal Tinkering Labs intends to set up 50,000 laboratories across government schools to develop innovation along with functional expertise.

- National Centres of Excellence in Artificial Intelligence with an outlay of ₹500 crore for educational purposes.

- Broadband connectivity to all government secondary schools and rural health centers.

- A ₹1 lakh crore Urban Challenge Fund works toward making cities growth centers.

- The government targets to invest ₹10 lakh crore through asset monetization programs and will execute the Jal Jeevan Mission for water supply initiatives.

Development in Exports:

- Digital infrastructure for international trade, such as BharatTradeNet.

- The government should work on establishing domestic industrial capacities which integrate globally while maintaining support for homegrown electronic products.

Financial Sector and Regulatory Reforms:

- The government plans to increase insurance foreign direct investment limits beyond 74% to reach 100%.

- The Jan Vishwas Bill 2.0 contains provisions to decriminalize more than 100 legal provisions.

- The expansion of the Investment Friendliness Index of States should be accompanied by a high-level committee dedicated to regulatory reforms in order to ease business operations.

Fiscal Management:

- The government expects a fiscal deficit at 4.8% for the financial year 2025 but aims to decrease it to 4.4% by the following year 2026.

- Government Expenditure: ₹50.65 lakh crore with an allocation of ₹1.5 lakh crore for state capital expenditure.

Welfare & Support Programs:

- PM Jan Arogya Yojana provides healthcare services to Gig Workers along with identity cards.

- Enhancement of support for elderly citizens involves increasing the threshold of ₹50,000 TDS deductions for interest income to ₹1 lakh.

Focus on Innovation and Education:

- Centre of Excellence in Artificial Intelligence for educational applications.

- Gyan Bharatam Mission for the survey and conservation of over 1 crore manuscripts and knowledge systems.

Trade & Industry:

- The government lowered Basic Customs Duty (BCD) tariffs for essential minerals and batteries as well as medical equipment and shipbuilding to boost national production.

- TCS on Rent: Raised from ₹2.4 lakh to ₹6 lakh.

Tax Simplification and Reforms:

- Self-Assessment Tax Returns: Extended time limit for updated returns from 2 to 4 years.

- TDS on Rent: Increased threshold for deductions to ₹6 lakh.

Exemptions & Reductions:

- Basic Customs Duty (BCD) exemptions on life-saving medicines and rare disease treatments.

- The Indian government judged strategic minerals crucial for battery and shipbuilding industries by removing Basic Customs Duty restrictions to maintain domestic capabilities.

Promoting Domestic Manufacturing:

- The manufacturing of fish products under an Inverted Duty Structure will benefit from lower Basic Customs Duty rates along with higher rates for interactive flat-panel displays built in India.

International Trade and Export Support:

- Sheep farmers benefit from BCD exemptions regarding wet blue leather products as part of their handicrafts and perishable item export initiatives.

Items That Got Cheaper

- Cancer & Rare Disease Drugs: 36 drugs exempt from Basic Customs Duty (BCD).

- Fish Products: BCD on fish paste reduced from 30% to 5%; BCD on fish hydrolysate reduced from 15% to 5%.

- Critical Minerals: Cobalt, lithium-ion battery scrap, and 12 minerals fully exempt from Basic Customs Duty (BCD)

- Platinum Findings: Basic Customs Duty (BCD) reduced from 25% to 6.4%.

- Shipbuilding Materials: Basic Customs Duty (BCD) on raw materials for ship manufacturing exempted for 10 years.

- Motorcycles: BCD on bikes ≤1600 CC reduced to 40% (from 50%); >1600 CC reduced to 30% (from 50%).

- Handicraft Exports: Exemption from BCD to boost exports.

- Wet Blue Leather: Full exemption from BCD to support leather exports.

Items That Got Costlier

- Knitted Fabrics: BCD increased to 20% or ₹115 per kg, whichever is higher.

- Interactive Flat Panel Displays: BCD increased to 20% from 10%.

About Budget:

As India's most significant financial statement the Union Budget outlines government projected revenues and spending programs during the years between April 1 to March 31. Under Article 112 of the Indian Constitution the "Annual Financial Statement" has been defined as the Budget while the Finance Minister delivers this document to Lok Sabha on February 1 annually. The government uses the Budget to define their financial strategies together with taxation proposals while setting their fiscal policies which support economic growth and stability and overall welfare.

Budget in Parliament

Each year the Finance Minister presents the Union Budget to Parliamentary members on February 1. The delivery happens first in Lok Sabha after which the Finance Minister delivers his budget speech about government fiscal policies and financial estimates. Parliament conducts multiple stages of examination on the budget following the speech until it gets transformed into an official law.

1. Introduction

- The Indian Constitution defines the budget as the "Annual Financial Statement" (Article 112).

- The term "budget" is not mentioned in the Constitution.

- The budget is a statement of estimated receipts and expenditures of the government for a given financial year, running from April 1 to March 31.

- The Union Budget is presented annually on February 1 by the Finance Minister in the Lok Sabha.

Historical Context

- The first Budget in pre-independent India was presented in 1860 by James Wilson, the then British Indian Government's Finance Minister.

- After independence, India’s first post-independence Budget was presented in 1947 by Finance Minister RK Shanmukham Chetty.

- John Mathai took over as Finance Minister after Sir Chetty’s resignation and presented the Union Budgets for 1949-50 and 1950-51.

- The 1949-50 budget marked the first budget for a unified India, incorporating all princely states post-independence.

Budget Preparation

- The Department of Economic Affairs, under the Ministry of Finance, is the nodal body responsible for preparing the Union Budget.

Budget Classification

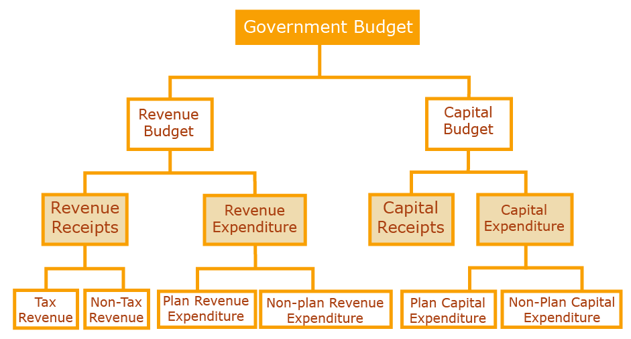

The Union Budget is divided into two primary sections:

- Revenue Budget: This includes the government’s expected income for the year, primarily through taxes, and covers day-to-day operating expenses.

- Capital Budget: This focuses on the government’s investments in assets, liabilities, and large-scale expenditures such as infrastructure development.

Structure of the Budget

- Part A: This section covers the macroeconomic overview, including government schemes, policies, and priorities for the year.

- Part B: This section includes the Finance Bill, which contains taxation proposals, such as revisions to income tax, and other fiscal measures.

Budget In Constitution of India

- Annual Financial Statement (Article 112)

- Demands for Grants (Article 113): Estimates of expenditure for various government ministries. These need to be approved by the Lok Sabha.

- Finance Bill (Article 110): A Money Bill that includes proposals for taxes and fiscal policies

Fiscal Policy Statements under the FRBM Act, 2003:

- Macro-Economic Framework Statement: Outlines key economic targets like GDP and fiscal deficit.

- Medium-Term Fiscal Policy cum Fiscal Policy Strategy Statement: Provides strategies to achieve fiscal targets.

🚀 "Union Budget 2025-26 is here! What are the key changes, tax updates, and economic impacts? Watch Bhuvnesh Sir’s in-depth analysis now!"

The content of the Budget consists of:

- Estimates of revenue and capital receipts

- Ways and means to raise revenue

- Estimates of expenditure

- Details of actual receipts and expenditures of the previous financial year, including reasons for any deficit or surplus.

Economic and financial policy for the upcoming year, which includes:

- Taxation proposals

- Revenue prospects

- Spending programs

- Introduction of new schemes and projects

Six Stages in Enactment of the Budget

- Presentation of the Budget: The Union Finance Minister presents the budget in Lok Sabha on 1st February each year, followed by a budget speech and laying it before both houses.

- General Discussion: Lok Sabha discusses the budget or any principle involved, but no cut motion or voting takes place. The Finance Minister responds at the end.

- Scrutiny by Departmental Committees: The demand for grants is scrutinized by departmental standing committees during a 3-4 week recess. They submit their report to the House afterward.

- Voting on Demand for Grants: Lok Sabha votes on each demand for grants. However, no voting is done on the expenditure charged on the Consolidated Fund of India.

- Passing of Appropriation Bill: An Appropriation Bill is passed to allow withdrawal from the Consolidated Fund of India for government expenses.

- Passing of Finance Bill: The Finance Bill is introduced to implement the government’s financial proposals for the next fiscal year.

Changes Introduced in 2017

- Advancement of Budget presentation to February 1 (earlier presented on the last working day of February),

- The merger of the Railway Budget with the General Budget, and

- Doing away with plan and non-plan expenditure.

Objectives of Government Budget

- Reallocation of Resources– It helps to distribute resources keeping in view the social and economic conditions of the country.

- Reducing Inequalities in Income and Wealth– Government aims to bring economic equality by imposing taxes on the elite class and spending the collected money on the welfare of the poor.

- Contributing to Economic Growth– A country’s economic growth is based on the rate of investment and savings. Therefore, the budgetary plan focuses on preparing adequate resources for investing in the public sector and raising the overall rate of investments and savings.

- Bringing Economic Stability– The Budget focuses on avoiding business fluctuations so as to accomplish the aim of financial stability. Policies such as Deficit Budget (during deflation) and Surplus Budget (during inflation) assist in balancing the prices in the economy.

- Managing Public Enterprises– Many public sector industries are built for the social welfare of the people. The Budget is planned to deliver different provisions for operating such business and imparting financial help.

- Reducing Regional Differences– It aims to reduce regional inequalities by promoting the installation of production units in the underdeveloped regions.

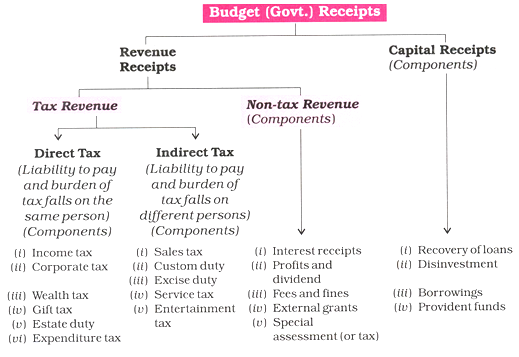

Components of Budget

Types of Budgets

Types of Budgets refer to different categories of government financial plans. The main types are Revenue Budget, which covers routine expenses like taxes and salaries, and Capital Budget, which focuses on long-term investments like infrastructure. Other types include Zero-Based Budgeting, where every expense is re-evaluated, and Outcome Budgeting, which measures the effectiveness of government programs. Gender Budgeting ensures financial resources are allocated to promote gender equality. These budgets help manage resources, promote stability, and address various social and economic goals.

1. Revenue Budget:

- Revenue Receipts: Income the government earns through taxes (e.g., excise duty, income tax) and non-tax sources (e.g., dividends, profits, interest).

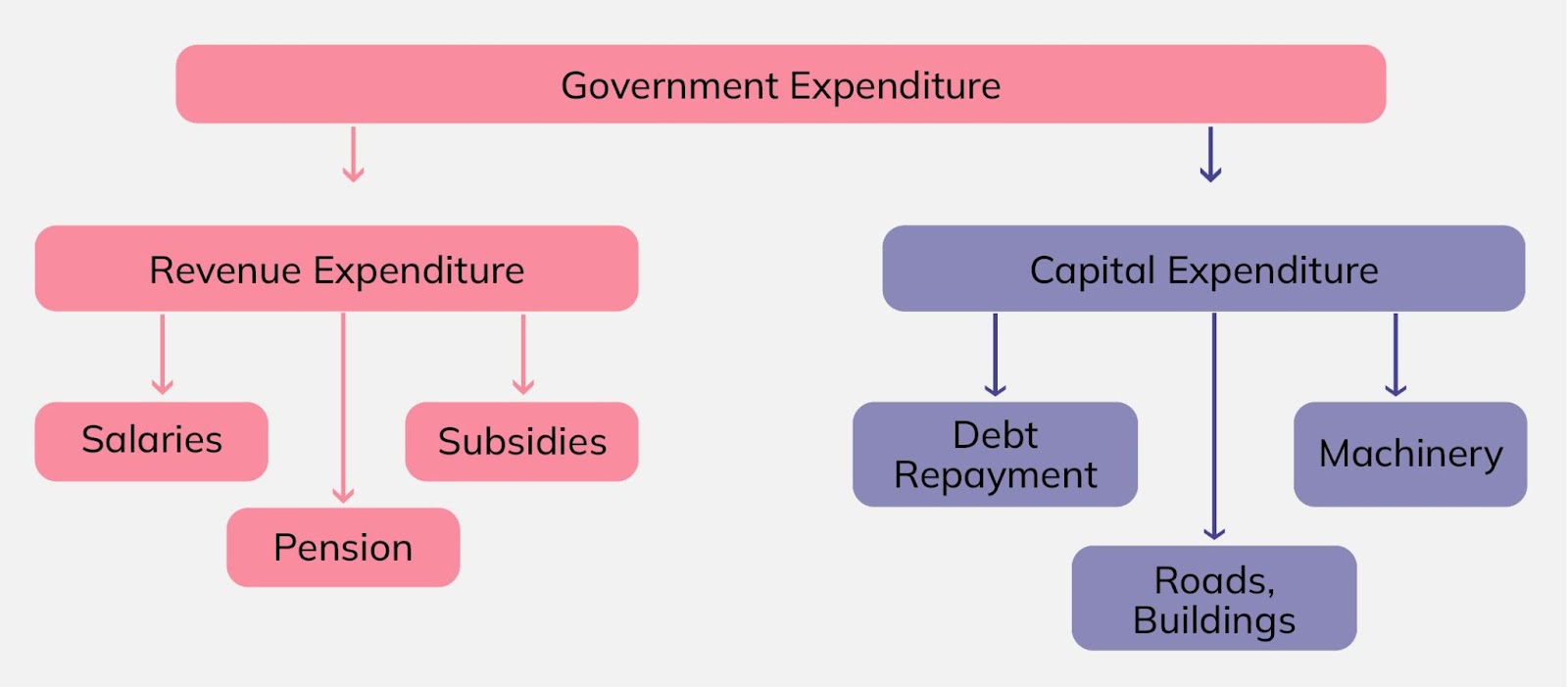

- Revenue Expenditure: Expenditure that doesn't affect government assets or liabilities, like salaries, pensions, interest payments, and administrative expenses.

2. Capital Budget:

- Capital Receipts: Receipts that lead to a decrease in assets or an increase in liabilities, such as funds from disinvestment (selling government assets) or borrowing.

- Capital Expenditure: Spending aimed at creating assets or reducing liabilities, such as investments in infrastructure or loans to states.

3. Other Types of Budgets:

- Zero-Based Budgeting: A method where every expense is evaluated from scratch, and each function is analyzed for its necessity and cost.

- Outcome Budget: Focuses on the results and impact of the budgeted funds. Introduced in 2005 to assess the outcomes of government programs.

- Gender Budgeting: Involves assessing and restructuring the budget to promote gender equality by allocating funds for female empowerment, welfare, and development programs.

4. Budget Types:

- Balanced Budget: When expenditure equals revenue for the fiscal year.

- Surplus Budget: When revenue exceeds expenditure (government has extra funds).

- Deficit Budget: When expenditure exceeds revenue, requiring borrowing to cover the gap.

5. Measures of Government Deficit:

Revenue Deficit: The excess of revenue expenditure over revenue receipts.

- Formula: Revenue Deficit = Revenue expenditure – Revenue receipts

Fiscal Deficit: The difference between the government’s total expenditure and its receipts (including non-debt receipts).

- Formula: Fiscal Deficit = Total expenditure – (Revenue receipts + Non-debt creating capital receipts)

Primary Deficit: The fiscal deficit minus interest payments. It shows the government's fiscal position excluding past debt obligations.

- Formula: Primary Deficit = Fiscal Deficit – Interest payments

6. Total Revenues and Types of Receipts

Total Revenues:

- This refers to the total amount of money a government can raise through various means.

- Key methods of raising revenues:

- Tax Revenues: Revenue generated by levying taxes (e.g., GST, income tax, corporate tax, excise duty, customs).

- Non-Tax Revenues: Includes income earned from non-tax sources, such as dividends from government-owned enterprises, fees, fines, and grants.

- Disinvestment Revenues: Money raised through the sale of public sector undertakings (PSUs) or government assets.

- Receipts: Types of Receipts:

- Revenue Receipts:

- These do not create liabilities for the government.

- Includes tax revenues (e.g., GST, income tax, etc.) and non-tax revenues (e.g., dividends, fees, fines).

- Non-Debt Capital Receipts:

- These receipts do not create future obligations or liabilities.

- Examples include:

- Recovery of loans (when the government collects previously given loans).

- Proceeds from disinvestment (selling government shares in PSUs).

- Debt-Creating Capital Receipts:

- These involve higher liabilities and create future repayment commitments.

- Examples include:

- Borrowings (government borrows money, increasing its future obligations).

- Loans raised by the government.

Conclusion

The Union Budget plays a crucial role in steering the country's economic and financial policies, aiming to balance the nation's priorities, such as growth, welfare, and stability. By carefully allocating resources across various sectors, it seeks to promote economic development, reduce inequalities, and ensure sustainable growth. The different types of budgets, including Revenue, Capital, and specialized ones like Gender Budgeting, enable the government to address diverse needs, from day-to-day expenses to long-term investments. Through a well-structured budget, the government aims to foster financial stability, support economic expansion, and improve living standards for all citizens.

Related Current Affairs

India’s Wheat Production Estimated to Hit Record High of 115.3 Million Metric Tonnes in 2024-25

India’s Wheat Production Estimated to Hit Record High of 115.3 Million Metric Tonnes in 2024-25 Surging Cotton Imports: Challenges for Indian Farmers & Textile Industry

Surging Cotton Imports: Challenges for Indian Farmers & Textile Industry India’s Spice Industry Needs Value Addition to Boost Global Market Share

India’s Spice Industry Needs Value Addition to Boost Global Market Share Govt Approves Multi-Feedstock Ethanol Plants for Sugar Mills

Govt Approves Multi-Feedstock Ethanol Plants for Sugar Mills India’s Bioeconomy to Reach $300 Billion by 2030: Union Minister

India’s Bioeconomy to Reach $300 Billion by 2030: Union Minister Jan Aushadhi Diwas 2025: Ensuring Affordable Medicines for All

Jan Aushadhi Diwas 2025: Ensuring Affordable Medicines for All Pradhan Mantri Shram Yogi Maandhan Yojana 2025: Pension Scheme for Unorganised Workers

Pradhan Mantri Shram Yogi Maandhan Yojana 2025: Pension Scheme for Unorganised Workers IRCTC and IRFC Attain 'Navratna' Status from the Government of India

IRCTC and IRFC Attain 'Navratna' Status from the Government of India India Needs Accelerated Reforms to Achieve High-Income Status by 2047: World Bank

India Needs Accelerated Reforms to Achieve High-Income Status by 2047: World Bank GeM: Revolutionizing Public Procurement with Transparency & Inclusion

GeM: Revolutionizing Public Procurement with Transparency & Inclusion